Why Most Organizations Aren't Funding Innovation

Without a clear definition, innovation investment is meaningless.

Twelve official definitions for R&D. Zero agreement.

The US government publishes at least a dozen distinct official definitions across agencies, accounting standards, tax authorities, and international bodies. Not one agrees with the others on where research ends and development begins.

Trillions of dollars flow through R&D budgets every year. Boards approve them. Investors evaluate them. Governments subsidize them. Analysts benchmark them. And the term at the center of all of it has no settled definition.

A company can gut its research investment without triggering a single alarm on its income statement. Researchers who gained rare access to confidential federal R&D data found exactly this: when companies face financial pressure, they cut research while leaving development essentially untouched, and the combined number barely moves. Every benchmark, every board conversation, every investment thesis built around the R&D line may be built on sand.

Innovation, ideas made real, requires both. Research is how you find the idea. Development is how you make it real. Strip out the research and you're not innovating, you're iterating on what already exists. Strip out the development and you're just experimenting. The problem is that nobody in the room knows which one they're actually funding, because the definition that would tell them doesn't exist.

Someone needs to draw the line. This episode is about why nobody has, and the definition I think should replace the chaos.

By the end, I'm going to put that definition in front of you and ask you to push back on it. Not to agree. To tell me where it breaks.

… or listen to the podcast.

How We Got Here

Four institutions took a run at defining R&D. Each one got it right for their own purposes. None of them got it right for yours.

Frascati: Built for Governments

In June 1963, OECD economists met at a villa in Frascati, Italy, south of Rome, and produced what became the international standard for measuring R&D across nations. Now in its seventh edition.

The Frascati Manual divides R&D into three tiers: basic research (theoretical work with no application in view), applied research (original investigation toward a specific practical objective), and experimental development (using existing knowledge to produce new products or processes). To qualify, an activity must be novel, creative, uncertain in outcome, systematic, and transferable.

Used by governments across roughly 75 countries. Solid for what it was designed to do: let nations compare R&D investment on consistent terms.

What Frascati cannot tell you: whether a specific company's spending is creating competitive advantage. It counts the type of activity. It doesn't assess what the activity produces for the organization doing the spending. A company can satisfy every Frascati criterion investigating something every competitor already knows. The knowledge is new to them. That is enough.

The accountants drew a different line, for a different reason, with a different consequence.

FASB: Built for Accountants

In October 1974, the Financial Accounting Standards Board issued Statement No. 2, Accounting for Research and Development Costs, now codified as Topic 730. Every public company filing under US GAAP operates under it.

The rule: all R&D costs expensed as incurred. Research, development, basic, applied: one line on the income statement. Their definition: research is a planned search aimed at discovery of new knowledge. Development is the translation of research findings into a plan or design for a new product.

The rationale is explicit in the original standard. Future benefits from R&D are, in FASB's language, "at best uncertain." Expense everything immediately. The standard solved the problem it was asked to solve, which was accounting treatment: when to recognize the cost, not whether the cost was strategically sound.

The consequence: sustaining engineering, feature maintenance, and incremental product updates all land on the same line as genuine exploratory research. Nobody looking at the income statement from outside can see the difference. The number is technically accurate and analytically opaque. Abraham Briloff, the late accounting professor at Baruch College, put it plainly: "Accounting statements are like bikinis. What they show is interesting, but what they conceal is significant." He was talking about financial reporting broadly. He could have been writing specifically about the R&D line. Researchers at Duke and London Business School spent years tracking corporate scientific output and found that it declined steadily across industries even as headline R&D spending kept rising. The combined number was hiding a substitution. Nobody on the outside could see it.

Outside the United States, a different standard governs, and it creates a comparison problem most analysts never account for.

IFRS: Built for International Investors

IAS 38 governs R&D under IFRS, and its treatment differs from FASB in one significant way.

Research costs are always expensed, same as FASB. But development costs can be capitalized as an asset on the balance sheet once a company can demonstrate technical feasibility, intent to complete, ability to use or sell the result, likely future economic benefit, adequate resources, and reliable cost measurement.

A European company that capitalizes its development phase carries those costs as an asset: lower expenses in the period, higher total assets. An identical US company expensing everything under FASB takes the full hit immediately: higher expenses, lower assets. Same underlying investment. Incomparable financial pictures.

Run the standard industry benchmark, R&D as a percentage of revenue, and you may conclude the US company is investing more aggressively. You may be comparing the same dollar invested under two different accounting regimes. Roughly 169 jurisdictions use IFRS. The United States does not. India uses an adapted version. Japan maintains its own standards board. The benchmark the industry trusts most is meaningless for cross-border comparison, and almost nobody says so.

Section 174: Built for Tax Authorities

The Internal Revenue Code adds another layer. Section 174 governs the deductibility of what the US tax authority calls "research or experimental expenditures," and the definition is not the same as FASB Topic 730.

A company's R&D for tax purposes and its R&D for financial reporting can cover different activities and produce different numbers. The Tax Cuts and Jobs Act of 2017 tightened this further: domestic R&D expenses that were previously deductible immediately now must be amortized over five years, international over fifteen. The definition of what qualifies shifted when the timing rules changed.

Within one country, one company, three definitional regimes apply simultaneously: Frascati for any government reporting, FASB for the income statement, and Section 174 for taxes. A single dollar of R&D spending can be classified three different ways depending on who's asking.

Enjoying this? Studio Sessions delivers innovation decision insights to your inbox.

The Gap None of Them Fill

Four frameworks, built by four institutions, for four different purposes. Not one was built for the question that actually matters.

Is this investment creating new knowledge that gives us a capability nobody else can easily replicate?

The gap between them is where innovation decisions actually live. The National Science Foundation recognized the problem clearly enough that it publishes a separate annotated document just to catalog the competing definitions, because they're too inconsistent to assume any two readers are using the same one. That gap isn't an oversight. It's a structural consequence of four institutions doing their own jobs well. The question practitioners need answered was nobody's institutional job.

You've been in the room. The R&D number is on the slide. Nobody asks what's inside it, because the accounting standard doesn't require an answer, and the room has learned not to expect one.

So it went unanswered. Until now.

A Better Definition for R&D

Here is my proposed definition:

Research is work directed at creating new knowledge where the outcome is genuinely uncertain and the knowledge cannot be readily obtained from existing sources. Development is the translation of that knowledge into products, services, or processes that meaningfully advance an organization's capability in ways competitors cannot easily replicate.

Four elements define it:

- Genuinely uncertain outcome. If you know what you're going to get before the work starts, it's engineering execution, not research. The uncertainty doesn't have to be total. Most applied research has a likely direction. But there has to be real doubt about whether the approach works, whether the knowledge emerges.

- Cannot be obtained from existing sources. This is the one nobody puts in writing. If the knowledge is already in the literature, available from a consulting engagement, or present in a competitor's published work, finding it again isn't research. Generating new knowledge and capturing existing knowledge are different activities. Only one belongs here. This criterion alone would reclassify a significant portion of what companies currently call R&D.

- Advances capability competitors cannot easily replicate. Development only qualifies when it translates research into something that genuinely moves the organization forward competitively. Sustaining engineering doesn't pass it. Feature parity doesn't. Competitive catch-up doesn't. All real work, none of it development under this definition.

- Agnostic to accounting jurisdiction. This definition doesn't tell you how to expense or capitalize anything. That's already governed by whichever standard applies. What it does is establish what genuinely belongs in each category, regardless of where the company files. That makes it usable across FASB and IFRS companies without translation.

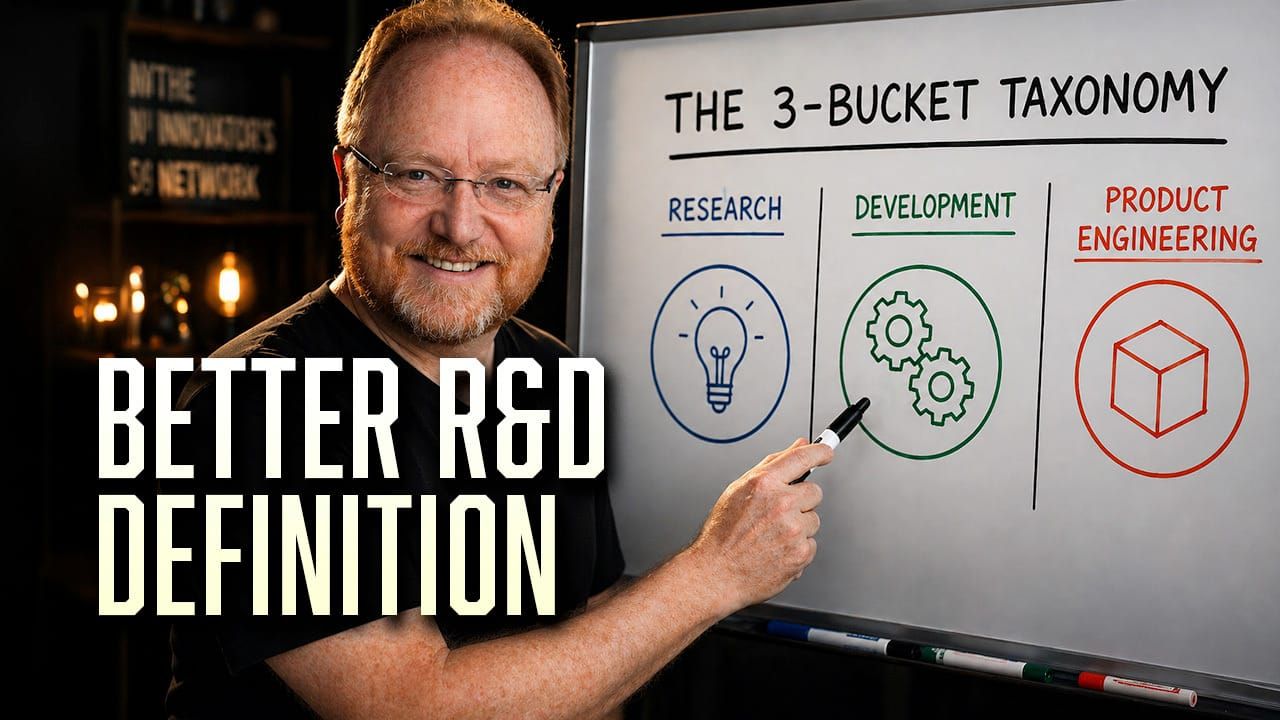

There is a simpler way to put it. For any project in your R&D budget, ask two questions. First: are we creating new knowledge, or executing against something we already know? If you're executing, it's not research. Second: does this translate into a capability competitors cannot easily replicate? If not, it's not development either. It's product engineering, valuable and necessary, but a different budget category entirely. Three buckets: Research, Development, and Product Engineering. That taxonomy, applied honestly across a typical portfolio, would reclassify a significant share of what most companies are currently reporting as R&D.

The Call

I'm not asking FASB to rewrite Topic 730.

What I am asking: that the people who actually make innovation decisions start applying a definition built for the question they're trying to answer.

If you run an R&D function: apply this definition to your current portfolio. Not to change the accounting. To see what's actually in the category and what isn't. The gap between what your budget calls R&D and what this definition calls R&D will tell you something worth knowing.

If you sit on a board: ask what portion of the R&D line is directed at new knowledge creation versus sustaining existing products. If no one in the room can answer, you're governing a number you don't understand.

And if you think the definition is wrong, tell me. Where should the line be drawn differently? What element doesn't hold? What did I miss? That's not a polite invitation. That's the actual point of this episode.

Definitions become standards when enough serious people apply them consistently and make the case until the institutions catch up. The four frameworks we inherited were each built by an institution serving its own purpose. This one is built for the people making the decisions.

The most consequential line in any company's budget is the one separating what builds the future from what protects the present. Nobody drew it clearly. It's past time someone did.

The idea was never the hard part. It never is. The call is.

If this episode shifted something for you, subscribe wherever you listen to podcasts. On YouTube, hit subscribe and the bell so you don't miss the next one.

And if you want to go deeper every Monday, subscribe to Studio Notes (FREE)

Innovation insights from Phil McKinney

Four decades of decisions. Delivered to your inbox.

Free or paid — your choice.

Produced by The Innovators Studio | philmckinney.com

Endnotes

- "at least a dozen distinct official definitions": National Center for Science and Engineering Statistics, "Definitions of Research and Development: An Annotated Compilation of Official Sources," NCSES 22-209 (Alexandria, VA: National Science Foundation, 2022). https://ncses.nsf.gov/pubs/ncses22209. The NSF publishes this document specifically because the definitions across federal agencies, accounting standards, tax authorities, and international bodies are too inconsistent to assume any two readers are working from the same one. The compilation covers Frascati, FASB Topic 730, OMB Circular A-11, Federal Acquisition Regulations, the Department of Defense's six-category RDT&E taxonomy, NCSES survey definitions, state government definitions, higher education definitions, nonprofit definitions, and international national accounts standards — confirming that the definitional landscape runs well beyond four frameworks.

- "researchers who gained rare access to confidential federal R&D data": Filippo Mezzanotti and Timothy Simcoe, "Research and/or Development? Financial Frictions and Innovation Investment," NBER Working Paper 31521 (August 2023). doi:10.3386/w31521. https://www.nber.org/papers/w31521. Using confidential Census Bureau BERD data with firm-level disaggregation — data not available to the public — the authors studied approximately 1,100 large US firms during the 2008 financial crisis. Companies facing refinancing pressure cut R&D, but the reduction was concentrated almost entirely in basic and applied research. Development spending remained essentially flat. Because the combined income statement line barely moved, the substitution was invisible to anyone outside the company. Mezzanotti is at the Kellogg School of Management, Northwestern University; Simcoe is at the Questrom School of Business, Boston University.

- "a villa in Frascati, Italy" / "three tiers" / "five criteria" / "roughly 75 countries": OECD, Frascati Manual 2015: Guidelines for Collecting and Reporting Data on Research and Experimental Development, 7th ed. (Paris: OECD Publishing, 2015). https://www.oecd.org/en/publications/frascati-manual-2015_9789264239012-en.html. The first edition was produced at the Villa Falconieri in Frascati, Italy, in June 1963, from a background document by Christopher Freeman. The three-tier taxonomy — basic research (§2.25), applied research (§2.29), experimental development (§2.32) — and the five criteria (novel, creative, uncertain in outcome, systematic, transferable/reproducible, §§2.6–2.8) have remained the core of the framework across all seven editions. The Manual's own estimate of international adoption reaches approximately 75% of OECD member countries for statistical reporting purposes.

- "Statement No. 2" / "at best uncertain" / "Topic 730": Financial Accounting Standards Board, Statement of Financial Accounting Standards No. 2: Accounting for Research and Development Costs (Stamford, CT: FASB, October 1974), now codified as Accounting Standards Codification Topic 730. The phrase "at best uncertain" describing the future benefits of R&D appears at SFAS No. 2, ¶41. The rule requiring all R&D to be expensed as incurred is at ASC 730-10-25-1. Companies are required to disclose the total R&D expense for each period but are not required to distinguish research from development, since both receive identical accounting treatment. The full FASB definitions are reproduced with permission in the NSF NCSES compilation cited in endnote 1. https://ncses.nsf.gov/pubs/ncses22209.

- "Accounting statements are like bikinis": Abraham Briloff, as cited in Ed Kless and Ron Baker, "Episode #101: Interview with Baruch Lev," The Soul of Enterprise podcast (February 2025). https://www.thesoulofenterprise.com/tsoe/lev. Briloff (1917–2013) was Professor Emeritus of Accounting at Baruch College, City University of New York, and a longtime critic of accounting standards. The observation is widely attributed to him in accounting literature and was cited by Baruch Lev of NYU Stern — the most prolific academic critic of intangibles accounting — in his discussion of financial reporting's concealment of R&D investment quality.

- "declined steadily across industries even as headline R&D spending kept rising": Ashish Arora, Sharon Belenzon, and Andrea Patacconi, "Killing the Golden Goose? The Decline of Science in Corporate R&D," NBER Working Paper 20902 (January 2015). doi:10.3386/w20902. https://www.nber.org/papers/w20902. Subsequently published as "The decline of science in corporate R&D," Strategic Management Journal 39, no. 1 (2018): 3-32. The paper documents a broad shift away from scientific research by large US corporations from 1980 to 2007, tracked through corporate scientific publications and patent output — measures of research output independent of any definitional framework. Publications by company scientists declined across industries even as total R&D spending rose. The value attributable to scientific research dropped while the value attributable to patents held steady, consistent with firms preserving development output while withdrawing from research investment. Arora and Belenzon are at Duke University's Fuqua School of Business; Patacconi is at the University of East Anglia (UEA) Norwich Business School.

- "capitalized as an asset" / "169 jurisdictions": International Accounting Standards Board, IAS 38 Intangible Assets, ¶¶54–57. The six capitalization criteria for development costs appear at IAS 38, ¶57: technical feasibility of completing the asset, intention to complete and use or sell it, ability to use or sell it, probable future economic benefits, availability of adequate resources, and reliable measurement of expenditure. IFRS Foundation, "Use of IFRS Accounting Standards by Jurisdiction" (2025). https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/. As of 2025, 169 jurisdictions require or permit IFRS for publicly accountable entities. Notable non-adopters include the United States (US GAAP), with India (Ind AS), Japan (Japanese GAAP with voluntary IFRS option), and China (CAS) operating under partially converged but distinct standards.

- "Section 174" / "amortized over five years": Internal Revenue Code §174, as amended by the Tax Cuts and Jobs Act of 2017 (P.L. 115-97). For tax years beginning after December 31, 2021, domestic R&D expenditures previously deductible immediately must be capitalized and amortized over five years; international R&D over fifteen years. Treasury Regulation §1.174-2 provides the governing definition of qualifying "research or experimental expenditure" under §174, which differs from both the FASB Topic 730 definition and the Frascati criteria — creating three distinct definitional regimes applicable simultaneously to a single company's R&D spending.

- "publishes a separate annotated document": National Center for Science and Engineering Statistics, "Definitions of Research and Development: An Annotated Compilation of Official Sources," NCSES 22-209 (2022). See endnote 1. The document's existence is itself evidence of the problem: the NSF found it necessary to publish a standalone reference cataloging the competing definitions precisely because they are too inconsistent for practitioners to navigate without a guide.

{kind=link}